This presentation discusses a method that incorporates the latest advances in the Bayesian constrained regression literature offering an alternative to the current Least Squares-based and Kernel Regression-based Stochastic frontier constrained estimation methods, both in terms of runtime and of data capacity.

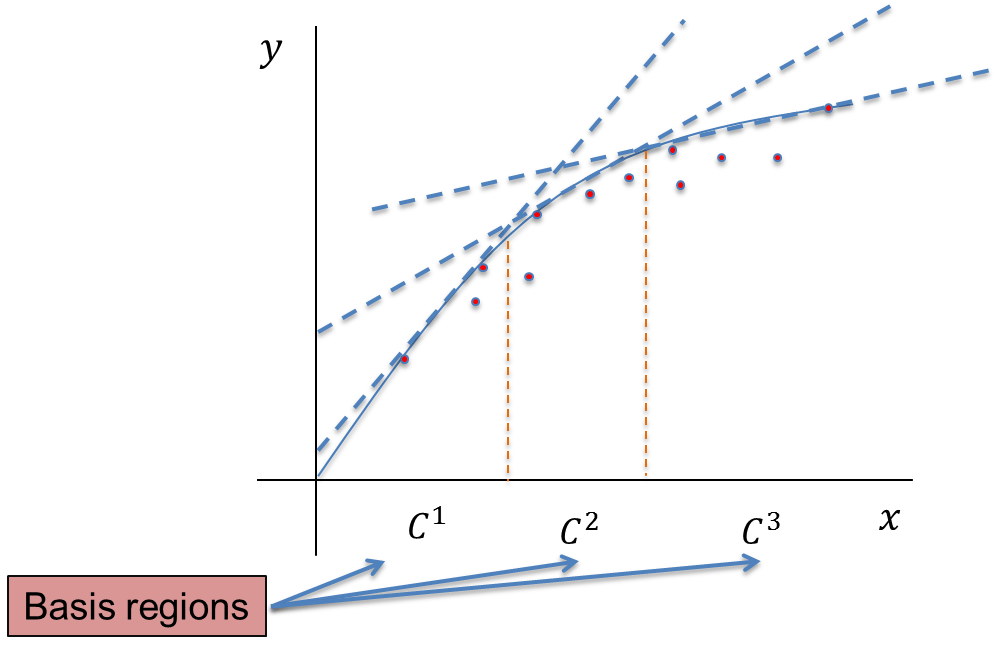

Although monotonicity constraints can be applied in a simple manner by the specification of sign constraints on the regression coefficients in both parametric and nonparametric settings, estimation of concavity-constrained production frontiers for flexible functional has proven to be more challenging. Imposition of such constraints in the nonparametric setting was discussed by Banker and Mandiratta (1992) and has been conducted using Least Squares approaches using Convex Nonparametric Least Squares (CNLS) (Kuosmanen, 2008). Du, Parmeter and Racine (2013) develop a Kernel regression method that also allows for imposition of a vast array of derivative-based constraints, including global concavity. This presentation discusses an extension to Multi-variate Bayesian Convex Regression (MBCR) developed by Hannah and Dunson (2013) to the setting with inefficiency. This extension offers benefits both in terms of runtime and of data capacity. Moreover, this method includes some extensions to the known Bayesian regression techniques and further enriches the Bayesian literature.